Sole Proprietorship vs Corporation: How To Choose

Explore sole proprietorship vs. corporation to choose the best business structure. Compare liability, taxes, costs, and more for informed decisions.

Starting a business is an exciting venture, but one of the first and most critical decisions entrepreneurs face is selecting the appropriate business structure. The choice between a sole proprietorship and a corporation significantly impacts liability, taxation, operational complexity, and growth potential. This comprehensive guide compares sole proprietorships and corporations, highlighting their benefits, drawbacks, and key considerations to help you make an informed decision tailored to your business goals.

Understanding Business Structures

A business structure defines how a company is legally organized, affecting everything from tax obligations to personal liability and fundraising capabilities. The two most common structures for new entrepreneurs are sole proprietorships and corporations. Each offers distinct advantages and challenges, and the right choice depends on factors like risk tolerance, financial goals, and long-term vision.

What Is a Sole Proprietorship?

A sole proprietorship is the simplest business structure, where an individual owns and operates the business without a legal distinction between the owner and the business. According to the IRS, a sole proprietorship is an unincorporated business owned by one person, making it the default structure for solo entrepreneurs who do not formally register their business as another entity.

What Is a Corporation?

A corporation is a separate legal entity created through a formal incorporation process, distinct from its owners (shareholders). Corporations can be classified as C corporations (C corps) or S corporations (S corps), each with unique tax and operational characteristics. Incorporation provides a legal barrier between the business and its owners, offering liability protection and other benefits but requiring more formalities.

Comparing Sole Proprietorship and Corporation

To choose between a sole proprietorship and a corporation, you need to understand their differences across key dimensions: setup, liability, taxation, control, costs, and growth potential. Below is a detailed comparison.

1. Setup and Complexity

Sole Proprietorship

- Ease of Setup: Sole proprietorships are the easiest to establish. No formal registration is required beyond obtaining necessary licenses or permits, which vary by location. For example, in Canada, registering a sole proprietorship with a service like Ownr costs around $49 and takes minutes.

- Maintenance: Minimal ongoing requirements. Owners file personal income tax returns, and no separate business filings are needed unless operating under a trade name.

Corporation

- Setup Process: Incorporating requires filing articles of incorporation with the state or provincial government, outlining the business’s structure, directors, and share allocation. In Canada, federal incorporation costs start at $200, while provincial fees can reach $350, plus additional costs for a business name search.

- Maintenance: Corporations face stricter regulations, including annual filings, shareholder meetings, and corporate minutes. These formalities demand time and resources, often requiring legal or accounting assistance.

2. Liability Protection

Sole Proprietorship

- Unlimited Liability: The owner is personally liable for all business debts, obligations, and lawsuits. If the business incurs debt or faces legal action, personal assets like homes, vehicles, or savings may be at risk.

- Risk Exposure: This structure suits low-risk businesses, such as freelance services, where legal or financial risks are minimal.

Corporation

- Limited Liability: A corporation shields owners’ personal assets from business liabilities. Debts or lawsuits against the business typically do not affect shareholders’ personal finances, making this structure ideal for high-risk ventures or businesses with significant assets.

- Exceptions: Limited liability is not absolute. Owners may still be liable for personal guarantees on loans or fraudulent activities.

3. Taxation

Sole Proprietorship

- Pass-Through Taxation: Business income is reported on the owner’s personal tax return, subject to individual income tax rates and self-employment taxes (e.g., Social Security and Medicare in the U.S., or CPP and EI contributions in Canada). This simplifies tax filing but can result in higher taxes if profits push the owner into a higher tax bracket.

- Deductions: Business losses can offset personal income, potentially reducing tax liability.

Corporation

- C Corporation: C corps face corporate income tax on profits, and shareholders pay personal taxes on dividends, leading to potential double taxation. However, corporations can deduct a wide range of business expenses, such as employee benefits, which may offset tax burdens.

- S Corporation: S corps avoid double taxation by passing profits and losses directly to shareholders’ personal tax returns, similar to sole proprietorships. However, S corps have strict eligibility criteria, including a limit of 100 shareholders and no non-resident alien shareholders.

- Tax Rates: Corporate tax rates are generally lower than personal rates. For example, in Canada, small business corporate tax rates are around 9–13% federally, compared to personal rates that can exceed 30%.

4. Control and Decision-Making

Sole Proprietorship

- Complete Control: The owner has full authority over all business decisions, from strategy to daily operations, without needing approval from partners or shareholders.

- Flexibility: This structure allows quick decision-making, ideal for solo entrepreneurs who value autonomy.

Corporation

- Shared Control: Corporations involve shareholders and directors, which can dilute the owner’s control, especially in larger entities. Decisions may require board approval or shareholder votes, potentially leading to conflicts.

- Structure: Corporations must adhere to bylaws and hold regular meetings, adding layers of governance.

5. Costs

Sole Proprietorship

- Low Startup Costs: Registration fees are minimal (e.g., $49–$100 in Canada, including name searches). Ongoing costs are limited to licenses, permits, and taxes.

- Affordability: Ideal for entrepreneurs with limited startup capital or those testing a business idea.

Corporation

- Higher Startup Costs: Incorporation fees range from $200 (federal) to $350 (provincial) in Canada, plus legal or accounting fees for drafting articles of incorporation or bylaws.

- Ongoing Costs: Annual filings, accounting services, and compliance costs can add up, often requiring professional assistance.

| Aspect | Sole Proprietorship | Corporation |

|---|---|---|

| Setup Cost | $49–$100 (e.g., Canada) | $200–$350 (Canada, plus legal/accounting fees) |

| Ongoing Costs | Minimal (licenses, taxes) | High (filings, compliance, professional fees) |

| Liability | Unlimited personal liability | Limited liability |

| Taxation | Personal income tax, self-employment tax | Corporate tax (C corp) or pass-through (S corp) |

| Control | Full control by owner | Shared with shareholders/directors |

| Complexity | Simple setup and maintenance | Complex setup and ongoing formalities |

6. Access to Capital

Sole Proprietorship

- Challenges: Raising capital is difficult as sole proprietorships cannot issue stock. Banks and investors may hesitate to lend due to unlimited liability and lack of formal structure.

- Funding Sources: Typically limited to personal savings, loans, or small grants.

Corporation

- Advantages: Corporations can raise funds by selling shares or issuing bonds, attracting investors and venture capital. Lenders often view incorporated businesses as more credible.

- Growth Potential: Easier access to capital supports expansion, hiring, or product development.

7. Perpetual Existence

Sole Proprietorship

- Limited Lifespan: The business ceases to exist if the owner dies, retires, or closes the business, as there is no legal separation between owner and business.

- Challenges: Transferring ownership is complex, often requiring a new business structure.

Corporation

- Perpetual Existence: A corporation continues to operate independently of its owners, facilitating ownership transfers or succession planning. This makes corporations suitable for businesses with long-term goals or legacy planning.

Alternative: Single-Member LLC

For entrepreneurs seeking a middle ground, a single-member limited liability company (LLC) combines elements of both structures. Available in the U.S. but not Canada (where a corporation serves a similar role), an LLC offers:

- Liability Protection: Like a corporation, it shields personal assets from business liabilities.

- Pass-Through Taxation: Income is reported on the owner’s personal tax return, avoiding corporate taxes.

- Simplicity: Less paperwork than a corporation but more than a sole proprietorship. Setup involves filing articles of organization and paying fees (typically $100–$800 in the U.S., depending on the state).

- Flexibility: Suitable for solo entrepreneurs who want liability protection without the complexity of incorporation.

However, LLCs may face dissolution in some states when a member leaves, unless an operating agreement specifies otherwise. They also require self-employment taxes, similar to sole proprietorships.

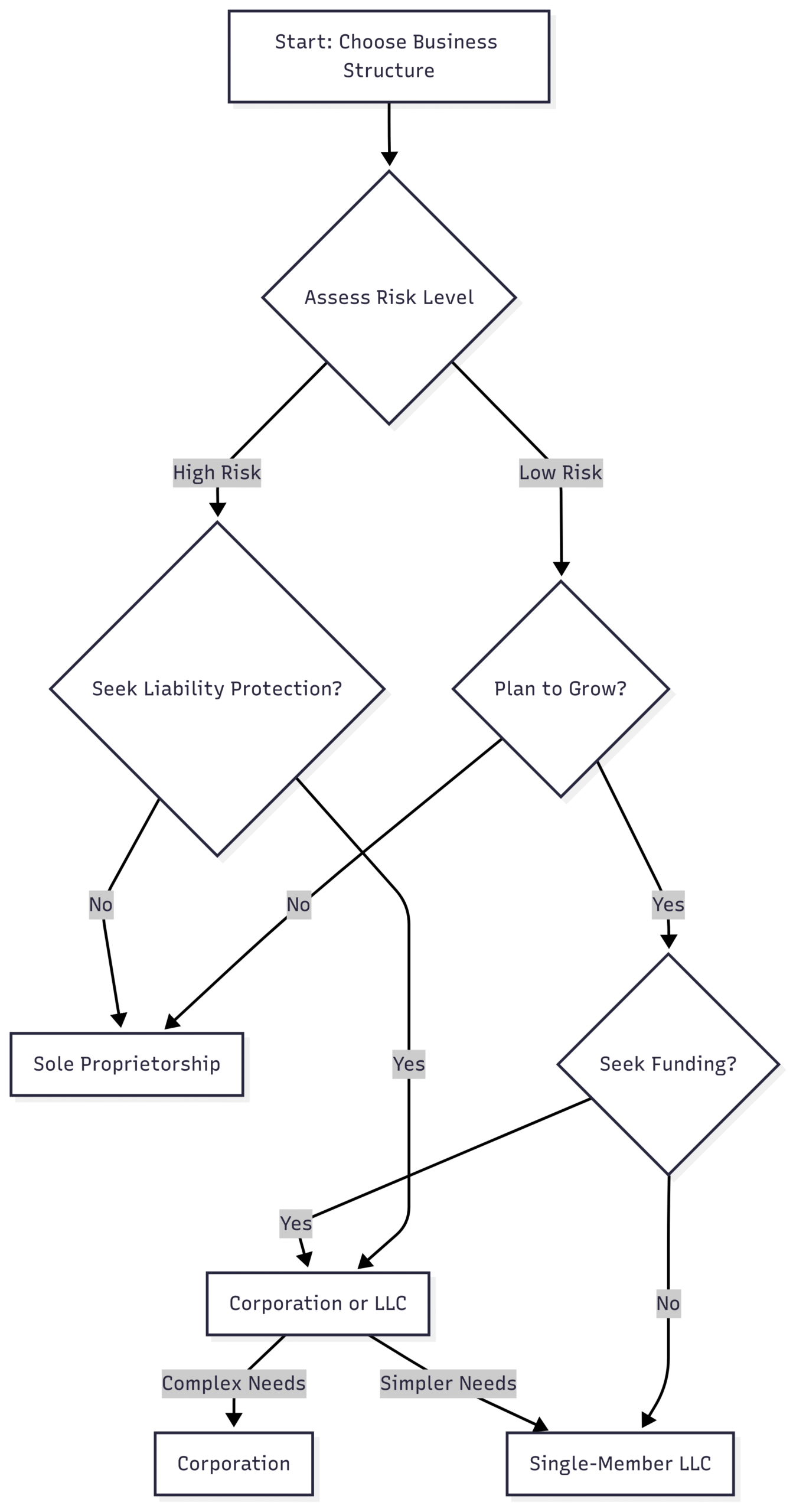

Chart: Decision-Making Flow

Below is a flowchart to guide entrepreneurs in choosing between a sole proprietorship, corporation, or LLC based on key factors.

This chart illustrates that low-risk businesses with minimal growth plans lean toward sole proprietorships, while high-risk or growth-oriented businesses benefit from corporations or LLCs.

Choosing the Right Structure: Key Considerations

Selecting a business structure requires evaluating your business’s needs, goals, and risk profile. Here are critical factors to consider:

1. Risk Tolerance

- Sole Proprietorship: Suitable for low-risk ventures like freelance services or consulting, where lawsuits or debts are unlikely. If you’re comfortable with personal liability, this structure is cost-effective and simple.

- Corporation: Ideal for businesses in high-risk industries (e.g., construction, manufacturing) or those with significant assets. Limited liability protects personal wealth from business risks.

2. Growth Plans

- Sole Proprietorship: Best for small, local businesses or side hustles with no plans for major expansion. Raising capital or transferring ownership is challenging.

- Corporation: Suited for businesses aiming to scale, attract investors, or go public. The ability to sell shares and transfer ownership supports long-term growth.

3. Tax Considerations

- Sole Proprietorship: Simplifies tax filing but may lead to higher taxes if profits are substantial. Consult a tax professional to assess whether pass-through taxation aligns with your income.

- Corporation: Offers tax advantages, especially for S corps, which avoid double taxation. Corporate deductions (e.g., health benefits, equipment) can reduce taxable income. However, C corps face double taxation unless structured as S corps.

4. Long-Term Goals

- Sole Proprietorship: Ideal for testing a business idea or operating a small venture with minimal overhead. It’s less suited for businesses with succession plans or legacy goals.

- Corporation: Supports long-term objectives like building a brand, expanding nationally, or planning for succession. Perpetual existence ensures the business outlives its founders.

5. Budget and Resources

- Sole Proprietorship: Low startup and maintenance costs make it accessible for entrepreneurs with limited funds.

- Corporation: Higher costs require a larger budget, but the investment may be justified by liability protection and growth opportunities.

Practical Steps to Get Started

For Sole Proprietorship

- Choose a Business Name: Use your legal name or register a trade name (e.g., “Jane’s Consulting”) with your state or province.

- Obtain Licenses/Permits: Check local requirements for business licenses, permits, or industry-specific certifications.

- Get a Tax ID: In the U.S., apply for an Employer Identification Number (EIN) if hiring employees or for banking purposes. In Canada, a Business Number (BN) may be required for GST/HST.

- Open a Business Bank Account: Separate personal and business finances to simplify accounting and tax filing.

- File Taxes: Report business income on your personal tax return (e.g., Schedule C in the U.S. or T2125 in Canada).

For Corporation

- Choose a Name: Conduct a name search to ensure availability and compliance with state/provincial regulations.

- File Articles of Incorporation: Submit documents to the state or federal government, including business name, address, directors, and share structure.

- Appoint Directors and Officers: Assign roles like president and secretary, ensuring compliance with residency requirements (e.g., 25% Canadian directors for Canadian corporations).

- Draft Bylaws: Outline governance rules, including shareholder meetings and voting procedures.

- Obtain an EIN/BN: Required for tax purposes and banking.

- Comply with Ongoing Requirements: File annual reports, hold shareholder meetings, and maintain corporate records.

Frequently Asked Questions

The primary advantage is simplicity. Sole proprietorships require minimal setup, low costs, and no complex filings, making them ideal for solo entrepreneurs starting small.

Unlimited liability exposes the owner’s personal assets to business debts and lawsuits, posing significant financial risk.

Generally, yes. Corporations benefit from lower corporate tax rates and additional deductions, though C corps may face double taxation. S corps and sole proprietorships both use pass-through taxation, but corporate structures offer more tax planning options.

Yes, a sole proprietorship can be incorporated later by filing articles of incorporation and restructuring the business. This transition may involve tax implications, so consult a professional.

An LLC provides liability protection and pass-through taxation, combining benefits of sole proprietorships and corporations. Sole proprietorships offer simplicity but no liability protection. LLCs are not available in Canada, where corporations serve a similar role.

Conclusion

Choosing between a sole proprietorship and a corporation is a pivotal decision that shapes your business’s legal, financial, and operational future. Sole proprietorships offer simplicity, low costs, and full control, making them ideal for low-risk, small-scale ventures or entrepreneurs testing an idea. Corporations provide liability protection, tax advantages, and growth potential but require higher costs and compliance efforts, suiting businesses with ambitious plans or higher risks.

Evaluate your risk tolerance, growth goals, tax situation, and budget before deciding. Consulting with a business advisor, accountant, or attorney can provide personalized guidance to ensure your choice aligns with your vision. Whether you opt for the straightforward path of a sole proprietorship or the structured benefits of a corporation, platforms like Ownr can streamline the setup process, letting you focus on building your business.

Please share this Sole Proprietorship vs Corporation: How To Choose with your friends and do a comment below about your feedback.

We will meet you on next article.

Until you can read, The 10 Best Tax Havens in Europe: Complete Guide