5 alternative bank account for digital nomad

Living without borders sounds liberating—until you try to send an invoice, withdraw cash in a new country, or watch 4% of your income disappear in bank fees every month. Traditional banks were built for people who stay put. Digital nomads are not those people.

The good news is that a new generation of fintech platforms and neobanks has emerged specifically for remote workers, freelancers, and location-independent professionals. These solutions eliminate the friction points that make traditional banking painful: foreign transaction fees, residency requirements, limited multi-currency support, and branch-dependent services.

This guide covers the five best alternative bank accounts for digital nomads, structured by use case so you can match the right tool to your actual situation.

Why Traditional Banks Fail Digital Nomads

Before diving into solutions, it helps to understand exactly where conventional banking breaks down for nomadic lifestyles.

Currency conversion costs are the most painful. Converting earnings from USD to a local currency through a traditional bank typically costs 3–5% per transaction. For someone earning $5,000/month, that’s $150–$250 lost every single month—before spending a cent.

Foreign transaction fees compound the problem. Most traditional banks charge 2–3% on every foreign purchase plus $3–7 per ATM withdrawal. In cash-heavy countries like Thailand, Vietnam, or Morocco, you might hit the ATM ten times a month.

Residency requirements create access barriers. Traditional banks in the US, UK, and Europe typically require local residency, a local address for correspondence, and in some cases, in-person verification. None of this works when you move every few weeks.

Account freezes are a real risk. Banks often flag cards used in rapid succession across multiple countries as fraud. Having your primary account frozen while abroad—especially in a country with limited English customer support—is a genuine crisis.

The right banking setup eliminates all of these pain points.

What to Look for in a Nomad-Friendly Bank

Not every “digital bank” is built equally. These are the features that actually matter:

- Multi-currency accounts: The ability to hold, receive, and convert between USD, EUR, GBP, and other major currencies without forced conversion at every transaction.

- Zero or near-zero foreign transaction fees: Non-negotiable. The difference between 0% and 2.5% compounds heavily over months of travel.

- Global ATM access or reimbursements: Especially critical in cash-dependent economies.

- No residency requirement: Essential for stateless nomads or those without a fixed tax home.

- Digital-first operations: Account opening, card management, transfers, and support all available through a mobile app.

- Reliable customer support: A frozen card or failed transfer in a foreign country with no live support is a nightmare scenario.

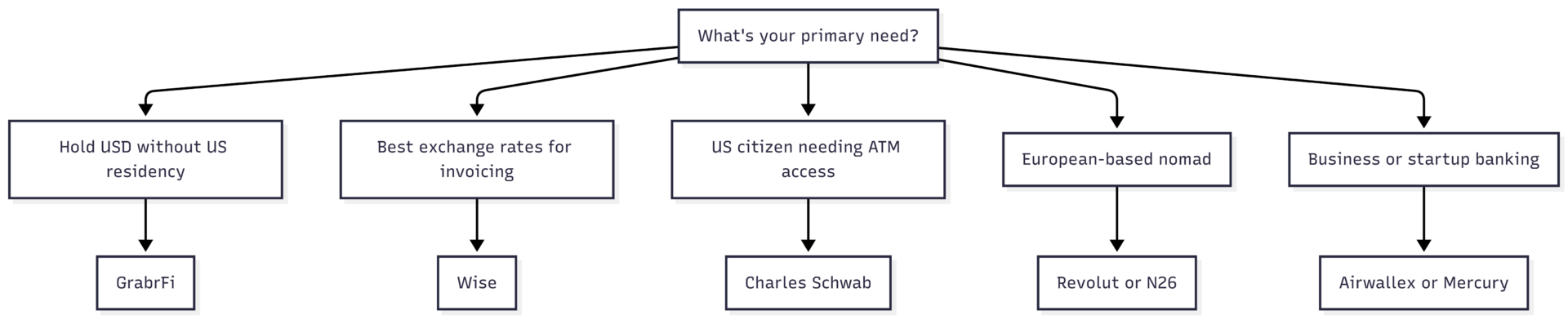

The 5 Best Bank Accounts for Digital Nomads

1. Wise — Best for Multi-Currency Invoicing

Wise (formerly TransferWise) has become the default recommendation for freelancers who bill clients in multiple currencies. Its core advantage is using the real mid-market exchange rate—the same rate you see on Google—rather than a marked-up “bank rate.”

How it works: Wise gives you local bank account details in USD, EUR, GBP, AUD, and several other currencies. When a US client pays your USD account, no conversion happens. You hold USD until you choose to convert, giving you control over timing and rate.

Key specs:

| Feature | Details |

|---|---|

| Currencies supported | 50+ |

| Conversion fee | 0.33%–1.5% (transparent, varies by currency pair) |

| ATM withdrawals | Free up to ~$100/month, then ~1.5% |

| Card type | Debit (Visa/Mastercard) |

| Residency required | No (available in 170+ countries) |

| Monthly fee | Free (card delivery ~$9 one-time) |

Best for: Freelancers and contractors invoicing international clients who want the best exchange rates and don’t need full banking features like direct deposit or checks.

Limitation: Wise is not technically a bank—funds are held in partner institutions, so deposit protection varies by country. It also lacks some traditional banking features.

2. Revolut — Best All-in-One for European Nomads

Revolut packs more features into a single app than any competitor: multi-currency accounts, budgeting tools, cryptocurrency trading, travel insurance (on premium tiers), and disposable virtual cards for online security. For European-based nomads, it’s often the only app they need.

Key specs:

| Feature | Standard (Free) | Premium ($9.99/mo) | Metal ($16.99/mo) |

|---|---|---|---|

| Currency exchange | Up to $1,000/mo at mid-market rate | Unlimited | Unlimited |

| ATM withdrawals (free) | $400/mo | $800/mo | $1,200/mo |

| Overseas medical insurance | No | Yes | Yes |

| Lounge access | No | No | Yes |

| Virtual cards | 1 | 5 | Unlimited |

Best for: European residents or nomads spending significant time in Europe who want a single app managing currency exchange, daily spending, travel perks, and budgeting.

Limitation: Customer service is app-only and can be slow. Some users have reported account freezes during verification processes. Availability and features vary significantly by country.

3. GrabrFi — Best for Non-US Residents Earning in USD

GrabrFi addresses a specific but extremely common nomad problem: you’re based outside the US, your clients pay in USD, but holding USD in your home country means your earnings immediately become subject to local currency volatility and conversion losses.

GrabrFi partners with a US-licensed bank to provide non-US residents with a real USD bank account—complete with US routing and account numbers—without requiring Social Security numbers or US residency.

What sets it apart is stablecoin integration. Beyond standard ACH transfers, GrabrFi supports receiving and sending USDC, USDT, and PYUSD, making it a bridge between traditional banking and crypto-native payment workflows. For freelancers paid partly in crypto, or those working with DAOs or Web3 projects, this matters.

Key specs:

| Feature | Details |

|---|---|

| Account type | USD checking (US routing + account number) |

| Primary markets | Argentina, Nigeria, Colombia (expanding) |

| Incoming ACH | $0 fee |

| Stablecoin support | USDC, USDT, PYUSD |

| Residency required | No |

| KYC process | Remote (passport + identity verification) |

Best for: Freelancers and remote workers in Latin America and Africa who earn in USD, want to protect earnings from local currency devaluation, and need efficient local withdrawal options. Also suited for anyone integrating stablecoin payments into their workflow.

Limitation: Currently focused on specific markets, so users outside supported regions may find limited local withdrawal functionality. Stablecoin features require additional compliance verification.

4. Charles Schwab — Best for US Citizens Traveling Long-Term

For American nomads who maintain US tax residency, Charles Schwab’s High Yield Investor Checking account is the gold standard for one simple reason: it reimburses every ATM fee, worldwide, at the end of each month. Every single one, with no cap.

In countries where visa-free stays require frequent border runs or ATM reliance is high, this saves meaningful money. Combined with zero foreign transaction fees on purchases, Schwab eliminates two of the biggest costs of travel banking entirely.

Key specs:

| Feature | Details |

|---|---|

| ATM fee rebates | Unlimited worldwide, end of month |

| Foreign transaction fee | 0% |

| Monthly fee | None |

| Minimum balance | None |

| Interest rate | Variable (linked to Schwab brokerage) |

| Requirement | US SSN + brokerage account (free to open, no funding required) |

Best for: US citizens traveling the world who want the simplest possible fee-free banking without multi-currency complexity. Ideal as a complementary account alongside Wise or GrabrFi.

Limitation: Requires US residency and Social Security number. Not useful for non-US citizens or multi-currency management. Account opening takes 1–2 weeks.

5. N26 — Best for European Nomads Wanting Simplicity

N26 is a German-regulated neobank with a clean, minimal interface and a zero-fee basic account. While Revolut has more features, N26 wins on simplicity and reliability for everyday euro-based banking.

Key specs:

| Feature | N26 Standard (Free) | N26 Smart ($4.90/mo) | N26 Metal ($16.90/mo) |

|---|---|---|---|

| Foreign transaction fee | 0% | 0% | 0% |

| ATM withdrawals (EU) | 3 free/month | 5 free/month | Unlimited |

| ATM withdrawals (non-EU) | 1.7% fee | 1.7% fee | Free |

| Travel insurance | No | No | Yes |

| Available | EU + US | EU + US | EU + US |

Best for: European residents or EU-based nomads who want a reliable, low-maintenance euro account with a clean interface and no minimum balance.

Limitation: Non-EU ATM withdrawals on lower tiers carry fees. Customer support is app-based. Less feature-rich than Revolut for multi-currency management.

Side-by-Side Comparison

| Bank | Best For | Multi-Currency | ATM Fees | Residency Required | Monthly Fee |

|---|---|---|---|---|---|

| Wise | Freelancers, invoicing | ✅ 50+ currencies | Limited free | No | $0 |

| Revolut | European nomads, all-in-one | ✅ 28+ currencies | Limited free | No (some limits by region) | $0–$16.99 |

| GrabrFi | Non-US residents earning USD | USD-focused | Depends on region | No | Varies |

| Charles Schwab | US citizens traveling | ❌ USD only | Unlimited reimbursement | US SSN required | $0 |

| N26 | European residents | Limited | 3 free/month (EU) | EU or US | $0–$16.90 |

How Most Nomads Actually Set Up Their Banking

Few nomads rely on a single account. The most common setups:

The Freelancer Stack: Wise for receiving client payments and holding multi-currency balances + Charles Schwab for fee-free ATM withdrawals + GrabrFi if operating in a currency-volatile market.

The European Nomad Stack: Revolut for daily spending and currency management + N26 as a stable euro base account + Wise for international transfers.

The Emerging Market Stack: GrabrFi for USD protection and stablecoin flexibility + a local mobile money service for day-to-day spending.

The key principle: never rely on a single account. Redundancy is insurance against freezes, technical issues, and coverage gaps.

Frequently Asked Questions

Yes, through fintech platforms like GrabrFi that partner with licensed US banks to offer accounts to non-residents. Traditional US banks require a Social Security number and local residency; these platforms have built compliant pathways around that requirement.

Traditional banks commonly freeze accounts that show activity across multiple countries rapidly. Modern neobanks and fintech platforms are designed for this—account freezes for normal nomadic travel patterns are far rarer. Always notify your bank when traveling long-term as a precaution.

No. Tax obligations are determined by your tax residency and citizenship, not where your account is held. However, US citizens must report foreign bank accounts annually via FBAR if balances exceed $10,000. Having a USD account through GrabrFi does not create US tax obligations for non-citizens.

Both Wise and GrabrFi provide US routing and account numbers that accept ACH transfers from Deel, Payoneer, and similar platforms. Always use ACH rather than wire transfer—ACH is typically free, while wire transfers can cost $15–$30 per transaction.

Yes, with digital-first platforms. GrabrFi, Wise, and Revolut allow account opening using your passport and home country documentation—no local residency proof required. Residency-restricted neobanks like the European version of N26 are exceptions; they require EU ID or a residency permit.

The right banking setup removes money from the list of things you have to think about while traveling. Start with the account that matches your primary use case—whether that’s holding USD abroad, minimizing conversion costs, or accessing cash fee-free worldwide—then add a secondary account as backup. The options above cover every major nomad profile, and most are free to open.

Please share these 5 alternative bank accounts for digital nomad with your friends and do a comment below about your feedback.

We will meet you on next article.

Until you can read, Belgrade gets you! Why digital nomads are drawn to the Serbian capital