What is the best online bank for travelling?

Using the wrong bank while travelling is an expensive mistake. Bank of America, Chase, and most traditional checking accounts hit you with foreign transaction fees of 2–3% on every purchase, ATM withdrawal fees of $3–7 per transaction, and wire transfer fees that can reach $45 for a single payment. On a two-month trip, these costs easily run into hundreds of dollars.

The solution isn’t to avoid spending—it’s to switch to a bank designed for travel. This guide breaks down the best online banks for travelling, compared by fee structure, ATM access, multi-currency features, and real-world usability.

What Makes a Bank Good for Travel?

Before comparing options, it helps to be clear about which features actually matter when you’re abroad.

Zero foreign transaction fees are the baseline. Any bank charging 2–3% per foreign purchase should be disqualified immediately. This fee compounds on every single transaction—coffee, groceries, accommodation, transport.

ATM fee reimbursements matter because cash is still unavoidable in many countries. Japan, Vietnam, Morocco, and much of Eastern Europe and Latin America remain heavily cash-dependent. A bank that reimburses ATM operator fees—not just waives its own—saves meaningful money.

No minimum balance requirements mean you’re not forced to park large sums in a low-interest account just to avoid monthly charges while traveling.

Mobile-first operations are non-negotiable. You need to freeze a lost card, update your address, check balances, and contact support—all from your phone, often in a different time zone.

Multi-currency support matters most for digital nomads, long-term travelers, and expats who earn or spend in multiple currencies. The ability to hold EUR, GBP, USD, and other currencies without forced conversion at unfavorable rates is a significant advantage.

Best Online Banks for Travel: Head-to-Head Comparison

1. Charles Schwab High Yield Investor Checking — Best for ATM Access Worldwide

Schwab is the most recommended travel checking account in traveler communities for one simple reason: unlimited ATM fee reimbursements, anywhere in the world, with no cap. When you withdraw cash from any ATM globally, Schwab reimburses the operator fee at the end of the month—every time, without exception.

Combined with zero foreign transaction fees, this eliminates the two biggest costs of using a debit card abroad.

One important note on ATM usage abroad: When a foreign ATM asks if you want to be charged in the local currency or your home currency, always select the local currency. Choosing your home currency triggers Dynamic Currency Conversion (DCC), which locks in a poor exchange rate controlled by the ATM operator—not your bank. Schwab reimburses the ATM fee but cannot override DCC if you accept it.

Specifications:

| Feature | Details |

|---|---|

| Monthly fee | $0 |

| Minimum balance | None |

| Foreign transaction fee | 0% |

| ATM fee reimbursement | Unlimited, worldwide |

| Interest (APY) | 0.05% (variable) |

| Linked account required | Schwab One brokerage (free, no funding required) |

| Cash deposit | Not available |

| FDIC insured | Yes, up to $250,000 |

Best for: US citizens and residents who travel frequently and want the most reliable, fee-free ATM access globally. Particularly strong in cash-heavy countries.

Limitation: Requires a US Social Security number. No multi-currency accounts—purely USD-focused. Account opening typically takes 1–2 weeks.

2. Wise — Best for Multi-Currency Management and Mid-Market Exchange Rates

Wise is the go-to solution for anyone who regularly transacts in multiple currencies. Rather than applying a marked-up “bank rate,” Wise uses the real mid-market exchange rate—the same one Google shows—and charges a small, transparent conversion fee (typically 0.33–1.5% depending on the currency pair).

What makes Wise especially useful for travellers is the local account details it provides. You get US routing and account numbers, a UK sort code and account number, a European IBAN, and equivalents for several other countries. Clients or employers can pay you as a local transfer, avoiding international wire fees entirely.

Specifications:

| Feature | Details |

|---|---|

| Currencies supported | 50+ |

| Conversion fee | 0.33%–1.5% (transparent, varies by pair) |

| Monthly fee | $0 (one-time card delivery ~$9) |

| ATM withdrawals | Free up to ~$100/month; ~1.5% after |

| Card type | Debit (Visa/Mastercard) |

| Residency required | No (available in 170+ countries) |

| Interest on balances | Available on select currencies |

| FDIC insured | Funds held with partner banks; protection varies |

Best for: Freelancers and travellers who invoice clients in multiple currencies, hold earnings in multiple currencies, or want consistently competitive exchange rates without hidden markups.

Limitation: Not a bank in the traditional sense—deposit protections vary by country. ATM access after free limits incurs fees. Some traditional banking functions are limited.

3. Revolut — Best All-in-One Travel App

Revolut packages multi-currency accounts, real-time exchange rates, budgeting tools, cryptocurrency trading, travel insurance, and virtual cards into a single app. For travellers who want one tool to handle everything, it’s the most feature-dense option available.

The core account is free and provides currency exchange at the mid-market rate during weekdays (a small markup applies on weekends). Premium tiers unlock higher ATM limits, unlimited currency exchange, lounge access, and comprehensive travel and medical insurance.

Plan Comparison:

| Feature | Standard (Free) | Premium ($9.99/mo) | Metal ($16.99/mo) |

|---|---|---|---|

| Currency exchange | Up to $1,000/mo, no markup | Unlimited | Unlimited |

| Free ATM withdrawals | $400/month | $800/month | $1,200/month |

| Overseas medical insurance | No | Yes | Yes |

| Priority support | No | Yes | Yes |

| Airport lounge access | No | No | Yes (2 visits/mo) |

| Disposable virtual cards | No | Yes | Yes |

Best for: European-based travellers or nomads spending significant time in Europe who want a comprehensive single app for currency management, daily spending, budgeting, and travel perks.

Limitation: Customer support is app-only and response times vary. Some users report account freezes during identity verification processes. Weekend currency exchange carries an additional fee. Availability and regulatory protections differ significantly by country.

4. Capital One 360 Checking — Best for Everyday Domestic and International Spending

Capital One 360 Checking has long been a strong option for travellers: zero foreign transaction fees, no monthly maintenance fees, no minimum balance, and access to over 70,000 fee-free ATMs through the Capital One, Allpoint, and MoneyPass networks.

Important update: Capital One has transitioned its debit cards from Mastercard to Discover. Discover acceptance internationally is significantly more limited than Mastercard or Visa, particularly in parts of Asia, Latin America, and smaller merchants across Europe. If you travel to regions with limited Discover acceptance, verify compatibility before relying on this card as your primary travel account.

Specifications:

| Feature | Details |

|---|---|

| Monthly fee | $0 |

| Minimum balance | None |

| Foreign transaction fee | 0% |

| Free ATM network | 70,000+ (Capital One, Allpoint, MoneyPass) |

| Out-of-network ATM reimbursement | None |

| Interest (APY) | 0.10% |

| Mobile app rating | 4.5+ stars (iOS and Android) |

Best for: US-based travellers who primarily spend on card and have access to the Capital One/Allpoint ATM network, and who are travelling in regions with strong Discover card acceptance.

5. Betterment Checking — Best for Full International ATM Reimbursement

Betterment is primarily known as a robo-advisor investment platform, but its checking account is quietly one of the best options for international travelers: it reimburses all ATM fees worldwide, including the fees charged by the ATM operator, with no monthly cap.

Additional perks include cash back at select retailers, cell phone insurance when you pay your bill with the Betterment debit card (up to $600 coverage), and zero overdraft fees.

Specifications:

| Feature | Details |

|---|---|

| Monthly fee | $0 |

| Minimum balance | None |

| Foreign transaction fee | 0% |

| ATM fee reimbursement | All ATM fees, worldwide, unlimited |

| Cash back | Yes, at select retailers |

| Cell phone insurance | Up to $600 (when bill paid with card) |

| Cash deposits | Not available |

| FDIC insured | Yes |

Best for: Travelers who want Schwab-level ATM reimbursements but prefer an account that also ties into an investment ecosystem. Note: requires direct deposit history for mobile check deposit eligibility.

6. UK and European Options: Starling Bank and Monzo

For UK and European residents, Starling Bank and Monzo are the top-rated travel accounts. Both offer zero fees for spending abroad and zero fees for cash withdrawals internationally (up to monthly limits), and both operate as fully licensed banks—not just e-money institutions.

Starling Bank is consistently rated highest among European travellers for its completely fee-free foreign spending and withdrawals, clean app, and 24/7 in-app customer support. Monzo offers similar features and is particularly popular among younger travellers for its budgeting tools and instant spending notifications.

These accounts are available to UK residents only. For European residents without UK access, Revolut and N26 are the primary alternatives.

Full Comparison Table

| Bank | Foreign Transaction Fee | ATM Reimbursement | Monthly Fee | Multi-Currency | Best For |

|---|---|---|---|---|---|

| Charles Schwab | 0% | Unlimited worldwide | $0 | No | US travelers, ATM access |

| Wise | 0% | Limited free monthly | $0 | Yes (50+) | Multi-currency, freelancers |

| Revolut | 0% (weekday) | Up to limit by plan | $0–$16.99 | Yes (28+) | European nomads, all-in-one |

| Capital One 360 | 0% | None (out-of-network) | $0 | No | US everyday spending |

| Betterment Checking | 0% | Unlimited worldwide | $0 | No | International ATM access |

| Starling Bank | 0% | Free (limits apply) | £0 | Limited | UK residents abroad |

| Fidelity CMA | 0% | Unlimited worldwide | $0 | No | US alternative to Schwab |

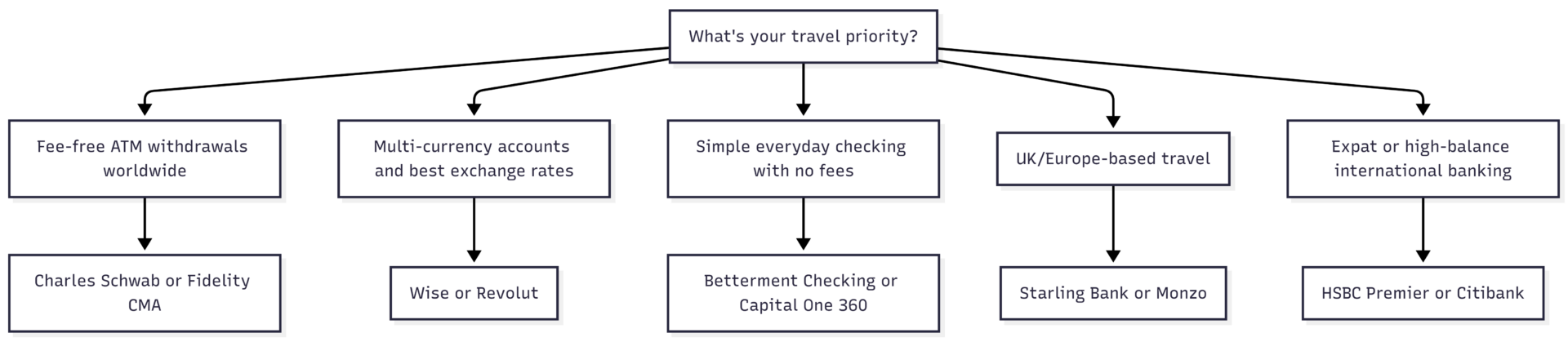

How to Choose the Right Account for Your Travel Style

The right account depends on how you travel and what you need most.

If you need cash frequently in countries where ATMs are the primary way to access money (Japan, Vietnam, Morocco, Eastern Europe), prioritize unlimited ATM reimbursements. Charles Schwab and Betterment Checking are the strongest options for US-based travelers. Fidelity Cash Management is a close alternative to Schwab that many users prefer for its faster fee reimbursement timing.

If you manage income in multiple currencies or bill international clients, Wise offers the best exchange rates and the most flexibility. You hold currencies without conversion and convert when rates are favorable.

If you want a single app to handle currency exchange, daily spending, budgeting, travel insurance, and more, Revolut’s premium tiers are worth the monthly fee for frequent travelers, particularly in Europe.

If you’re a UK resident, Starling Bank is the straightforward choice—it’s a fully licensed bank with zero foreign fees and strong customer support.

Most experienced travelers use two accounts: one for ATM access (Schwab or Betterment) and one for currency management (Wise or Revolut). Redundancy protects you if one card is frozen, lost, or not accepted at a specific merchant.

Frequently Asked Questions

Charles Schwab, Wise, Revolut, Capital One 360, Betterment Checking, and Fidelity CMA all charge zero foreign transaction fees on debit card purchases abroad.

Yes. Schwab reimburses ATM operator fees charged anywhere in the world, credited to your account at the end of each month. There is no cap on reimbursements.

Wise is not a bank—it’s a licensed financial services company. Your funds are held with partner banks and protected according to the regulations in your country of residence. In the US, funds are held in FDIC-insured partner banks.

Capital One transitioned its debit cards from Mastercard to Discover. Discover has significantly more limited international acceptance, particularly in Asia and parts of Latin America. This makes Capital One 360 less reliable as a primary travel card than it previously was.

No. Charles Schwab requires US residency and a Social Security number. Non-US residents should use Wise, Revolut, or GrabrFi (for USD accounts without US residency) instead.

Both have a role. A travel credit card with no foreign transaction fees is better for everyday purchases since it offers stronger fraud protection—disputed charges on credit cards are easier to resolve than debit card fraud. A debit card from Schwab or Betterment is better for cash withdrawals. Using both gives you flexibility and a backup if one fails.

Please share this What is the best online bank for travelling? with your friends and do a comment below about your feedback.

We will meet you on next article.

Until you can read, 5 alternative bank account for digital nomad